Primis Mortgage

Market Update

by Greg Richardson, Primis Mortgage EVP – Capital Markets

Rates Plummet as The Market Buys into the Big Shift

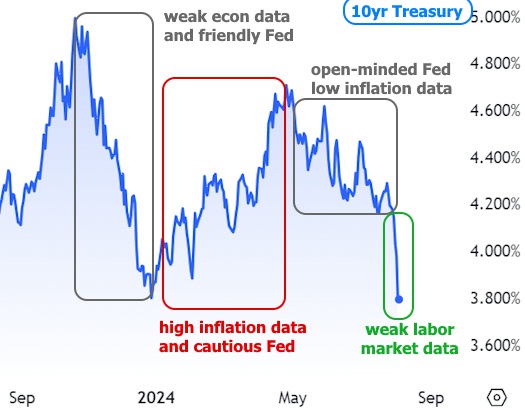

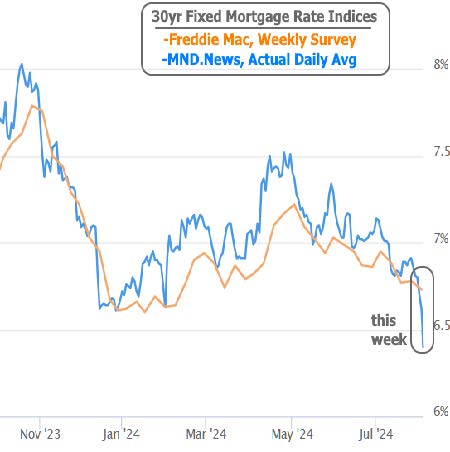

The events of this past week serve as an exclamation point in one of the many sentences that tells the story of the big shift away from the generationally high rates seen at the end of 2023. The story has had its ups and down since then, but it had been going fairly well for fans of low rates over the past 3 months.

In fact, the last 3 months mark the first successful defeat of what had looked like yet another “false start” in the road toward lower rates. Measured in terms of 10yr Treasury yields, long term rates have only made 3 attempts to drop more than half a percent since they began skyrocketing in 2022. The first two attempts ultimately gave way to new highs. If rates had moved just a bit higher a few months ago, it would have happened again.

Zooming in on the past year, here’s a general breakdown of the key motivations for these swings:

May through July could be described as cautiously optimistic due to well-received improvements in inflation data. During this time, the Fed said it was feeling more and more confident about cutting rates, but that it could be patient due to a labor market that was still rather strong. Similar sentiments were shared by the Fed as recently as this week, but that was before this week’s jobs report came out.

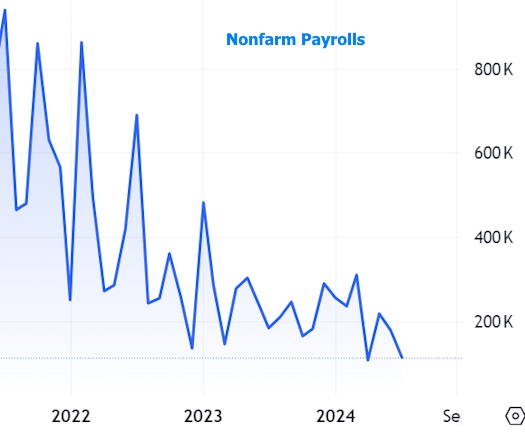

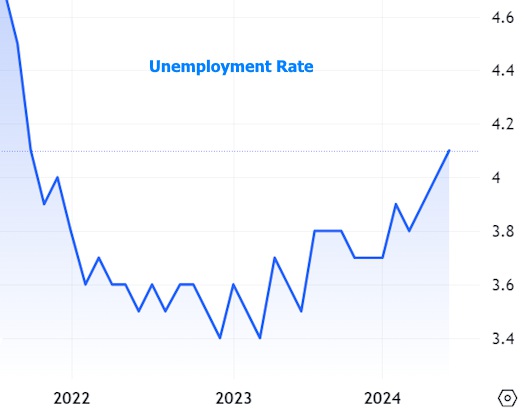

Headline job creation (nonfarm payrolls) fell to 114k in July–well short of the forecast consensus of 175k. In addition, the unemployment rate ticked up to 4.3% from 4.1% and wage growth fell to 0.2% from 0.3% with annual growth hitting pre- pandemic levels for the first time since stabilizing at long-term highs.

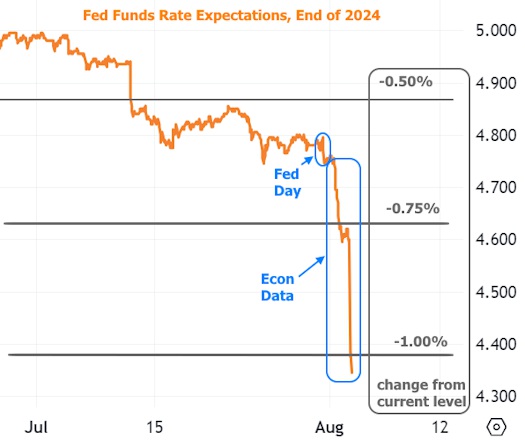

Bonds and rates were already in good spirits due to bad economic news on Thursday (higher Jobless Claims data and a weaker ISM Manufacturing Index), but the jobs report took the rally to the next level. Here’s how it looked in terms of expectations for the Fed Funds Rate by the end of 2024 (notably, Wednesday’s Fed announcement had very little impact on the outlook compared to Thu/Fri econ data):

In other words, traders were expecting the Fed to be able to cut rates by half a percent before this week, but now see at least a full point of cuts. At times like this, short term rates move much more than longer term rates like mortgages. Even so, Friday was one of only a few days in the past 2 decades with as big of a single day drop in average mortgage rates.

It’s very fair to ask where we go from here. There is never a crystal ball and the lessons of early 2024 should be kept in mind. Additional improvement in rates will require a fresh supply of downbeat economic data and there aren’t many big ticket reports on the horizon. Apart from Monday’s ISM Services Index, we’ll be waiting until the following week for the next installment of the Consumer Price Index (CPI)–the only other report that’s as big of a deal as the jobs report these days.

Beyond the next 2 weeks, the next month and a half could be particularly volatile. As it stands, the market is second-guessing the Fed’s decision to hold steady this week and wondering if they’ll be playing catch-up in mid-September in the event econ data keeps trending weaker.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Information is provided by MBS Live, LLC.