October 31 – November 4, 2022

Market Wrap Up

by Gregory Richardson | Primis Mortgage EVP – Capital Markets

Higher Rates Due to The Fed, But Not Due to The Fed’s Rate Hike

The Federal Reserve hiked rates by 0.75% this week and 30yr fixed mortgage rates moved moderately higher. Interestingly enough, those two things are fairly unrelated.

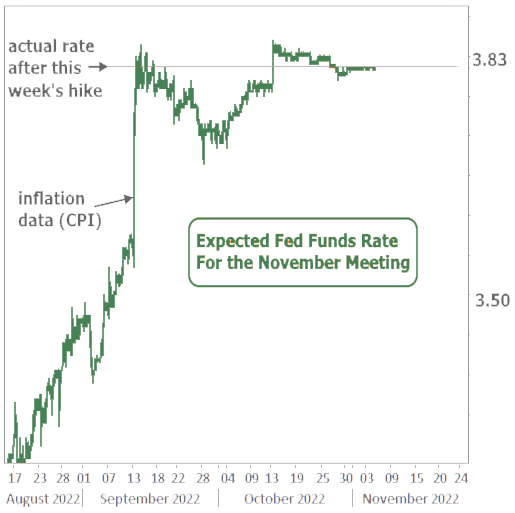

The Fed Funds Rate (the thing the Fed “hikes” when you hear about the Fed hiking rates) applies to overnight loans among large financial institutions. It’s important, to be sure, but it only changes 8 times a year whereas securities in the bond market change every second of the day.

There are all kinds of bonds. US Treasuries are the quintessential example. The yield on a 10yr US Treasury is the most popular benchmark for longer-term interest rates in the world. There are bonds that underlie the mortgage market as well (MBS or mortgage-backed-securities). They tend to move a lot like US Treasuries. There are even bonds that traders use to bet on the future level of the Fed Funds Rate (incidentally called “Fed Funds Futures”).

With that in mind, the bond market has LONG since assumed the Fed would hike 0.75% this week. The Fed Funds Futures contract for November was locked into the new rate since late last week and first reached that level in mid September after the CPI inflation data.

All that to say that new of a 0.75% rate hike isn’t really news. Markets have known and had already adjusted. In fact, when the hike was announced, rates actually IMPROVED for several minutes.

The improvements were possible because when the market is already certain of the rate hike outcome, it focuses its reaction on any changes in the WORDS of the policy statement that the Fed releases along with the rate hike. In this week’s case, traders were hoping to get some indication that the Fed was getting close to having a discussion about slowing the pace of rate hikes. This is essentially the “pivot” concept we discussed last week (get caught up here if you missed it).

While it was very carefully worded, Wednesday’s announcement actually included an allusion to pivot potential. This was a surprise for many market participants. Most felt that the pivot would be discussed by Fed Chair Powell in the press conference that follows the announcement 30 minutes later. It was this verbiage change that enabled the brief bond market rally (note: bond rallies imply lower rates, all other things being equal).

“In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

That’s the Fed’s way of saying it realizes there have been a lot of hikes already and that it could take some time for those hikes to have an impact on inflation, thus opening the door for them to consider hiking more slowly going forward. Indeed, we would hear several Fed speakers confirm this by Friday, saying that 0.50% hikes would be just as effective, but the market needs to know that there could simply be more of them!

If the statement was the extent of Wednesday’s communication, bonds/rates would have had a solid enough week, but remember that press conference with Fed Chair Powell? That didn’t go so well, and not for any complicated reasons.

While Powell acknowledged the Fed would discuss slowing the pace of hikes, he was very clear in saying the fight against inflation was far from over. Specifically, he said there was no indication that inflation is coming down and that it’s not time to even discuss the notion of “pausing” rate hikes. He also said that the Fed members’ individual rate hike forecasts in December were likely to be higher than they were in September. The press conference ended with him saying inflation was becoming more and more challenging to deal with, and that required more restrictive policy.

Markets don’t like more restrictive policy, even if the goal ideally better for markets in the long run. Stocks slid and rates spiked on that news. Most mortgage lenders issued mid-day rate increases. The change wasn’t extreme in the context of other recent moves, but it was nonetheless not what anyone was hoping to see after the coast looked to be clear after the initial policy announcement.

This week’s volatility aside, the more important events for bonds/rates are yet to come. The Fed, after all, is only responding to changes in economic data when deciding on its rate hike pace. The most important report to watch in that regard is the Consumer Price Index (CPI), which will be out next Thursday.

A note on this week’s rate headlines:

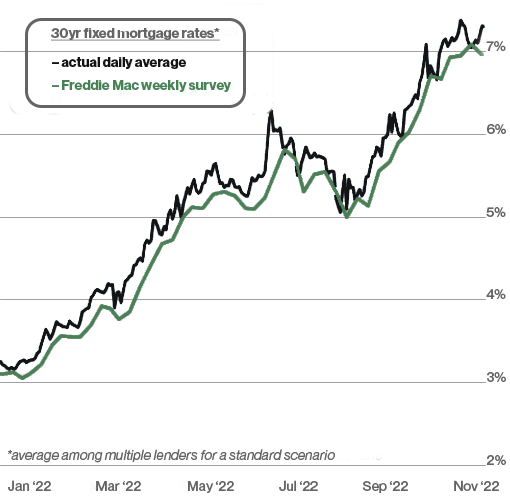

Multiple news outlets cited lower rates this week, but those news stories are based on stale data. Freddie Mac’s weekly mortgage rate survey comes out on Thursday, but only really measures Monday and Tuesday. This week, that meant comparing the lowest rates of this week to last week’s highest rates. But rates had already fallen by the end of last week and then spent most of this week moving higher. If the Freddie survey were a day to day number, it would be back up in the low 7% range as opposed to the high 6’s

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Information is provided by MBS Live, LLC.