Primis Mortgage

Market Update

Written by Greg Richardson, Primis Mortgage EVP – Capital Markets

Biggest Weekly Jump for Rates in Quite a While. Will it Keep Going or Calm Down?

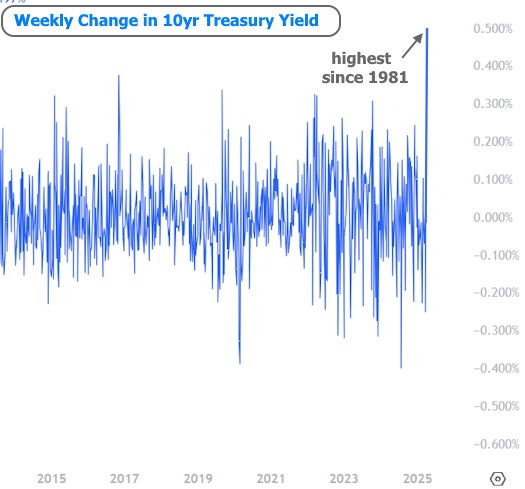

HeWhether we’re talking about mortgage rates or a quintessential yard stick of the rate world like the 10yr Treasury yield, it was the roughest week in quite a while.

Nearly every corner of the market continues reacting in volatile fashion to last week’s tariff announcement and the subsequent updates. Momentum toward higher rates took on a life of its own this week for laundry list of mostly esoteric reasons.

Meanwhile, the typical sources of market inspiration fell on deaf ears. Notably, both of this week’s inflation reports were much lower than expected. That would typically be great news, but instead, rates kept on moving relentlessly higher.

When it comes to 10yr Treasuries, you would need to go back to 1981 to see a bigger jump.

Is this alarming? Does it suggest that some massive shift is taking place that will re-write the global economic order?

Some would say yes. Others would laugh. Many would be somewhere in between with quite a few qualifying ideas. No one would deny that the answer ultimately depends on things that have yet to happen.

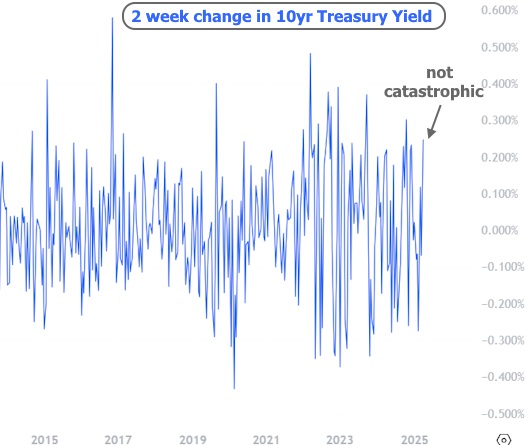

One great way to find some perspective is to consider the 1-week chart of 10yr Treasury yields above against a 2-week chart below. In other words, it’s the exact same data, but over a 2-week time frame instead of week-over-week. Spoiler alert: it’s not ideal, but definitely not as alarming as the first chart.

With that in mind, there’s a lot riding on the coming week and a half to flesh out the bigger picture. In the meantime, mortgage rates are definitely elevated–much more so than the typical news article has yet conveyed.

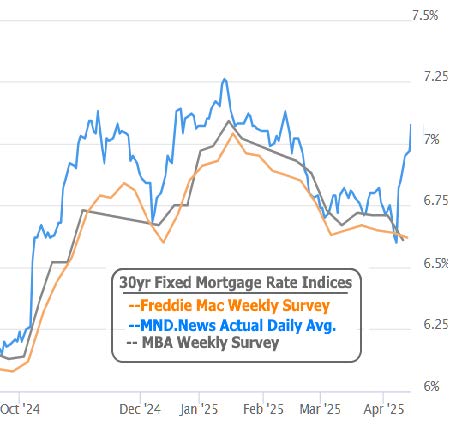

In the chart above, it’s normal for the blue line to generally operate above the other two. The important observation is the extent to which big moves in the blue line (actual daily average rates) lead subsequent moves in the other lines (surveys that have a reporting lag). Unfortunately, many news outlets report on the weekly surveys as if those rates are still available.

Instead, they’re just a look back to what was available last week.

Here too, there’s perspective. After all, mortgage rates were noticeably higher just a few months ago. Moreover, we’ve certainly seen a few weeks with a 0.50% jump over the past few years. So the question remains: will the coming weeks add insult to injury, or will they help mellow out the bigger picture message? The answer can’t be known today. The best bet is to understand the potential for additional volatility and be prepared to react accordingly.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Information is provided by MBS Live, LLC